INSURANCE SUBSCRIPTION

INSURANCE SUBSCRIPTION

PREDICTION

STATA SOURCE CODE

STATA SOURCE CODE

Description & Objectives

Description & Objectives

TEST OF INDEPENDENCE ON QUALITATIVE VARIABLES

TEST OF INDEPENDENCE ON QUALITATIVE VARIABLES

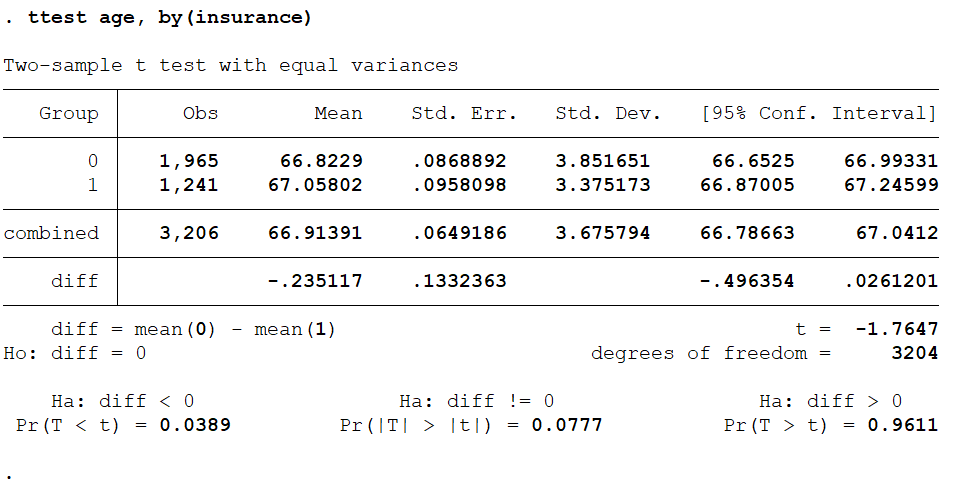

MEAN COMPARISON TEST

MEAN COMPARISON TEST

LOGIT MODEL ESTIMATION

LOGIT MODEL ESTIMATION

RESULTS ANALYSIS

CALCULATING MARGINAL EFFECTS

CALCULATING MARGINAL EFFECTS

ELASTICITY AND SEMI-ELASTICITY

Prediction Quality Analysis and Error Rate

Forecast

Forecast